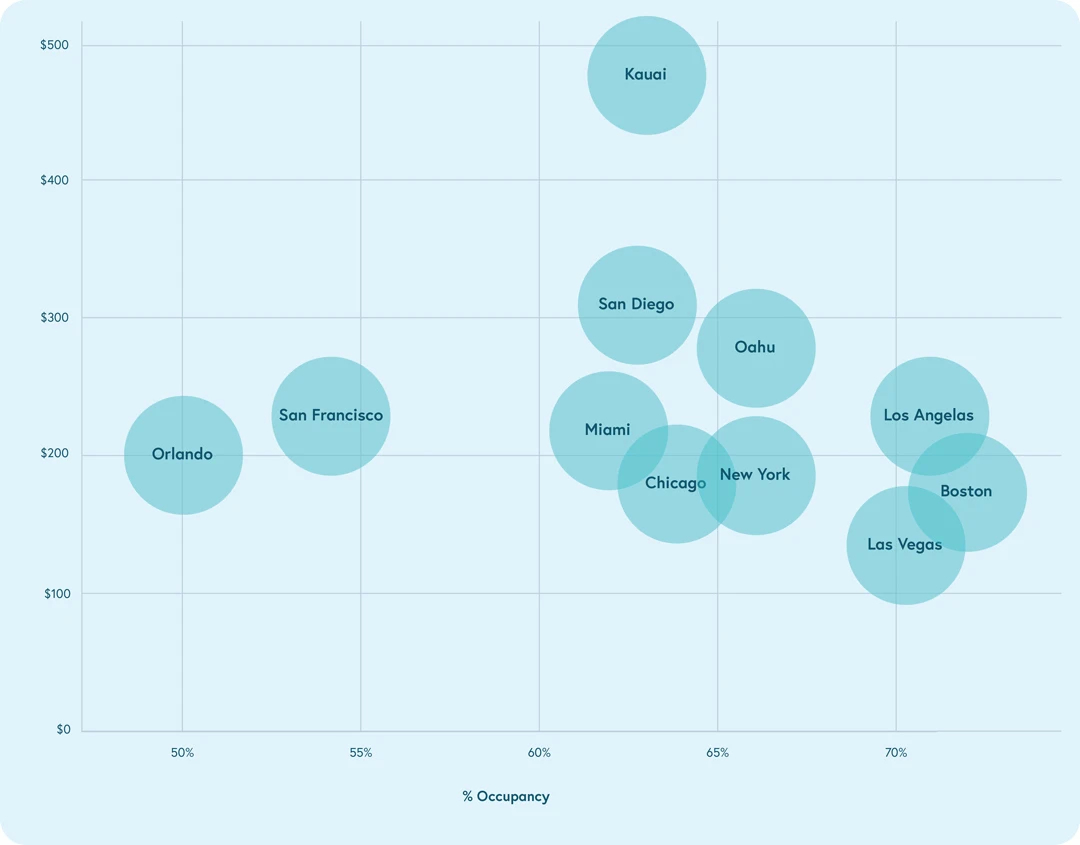

While there were a number of hot markets across the entire US, as evidenced by the chart above, Beyond chose to dive deep into three markets that have the potential for particularly interesting growth. To learn more about what Beyond’s data is showing for your specific market,

contact us here.