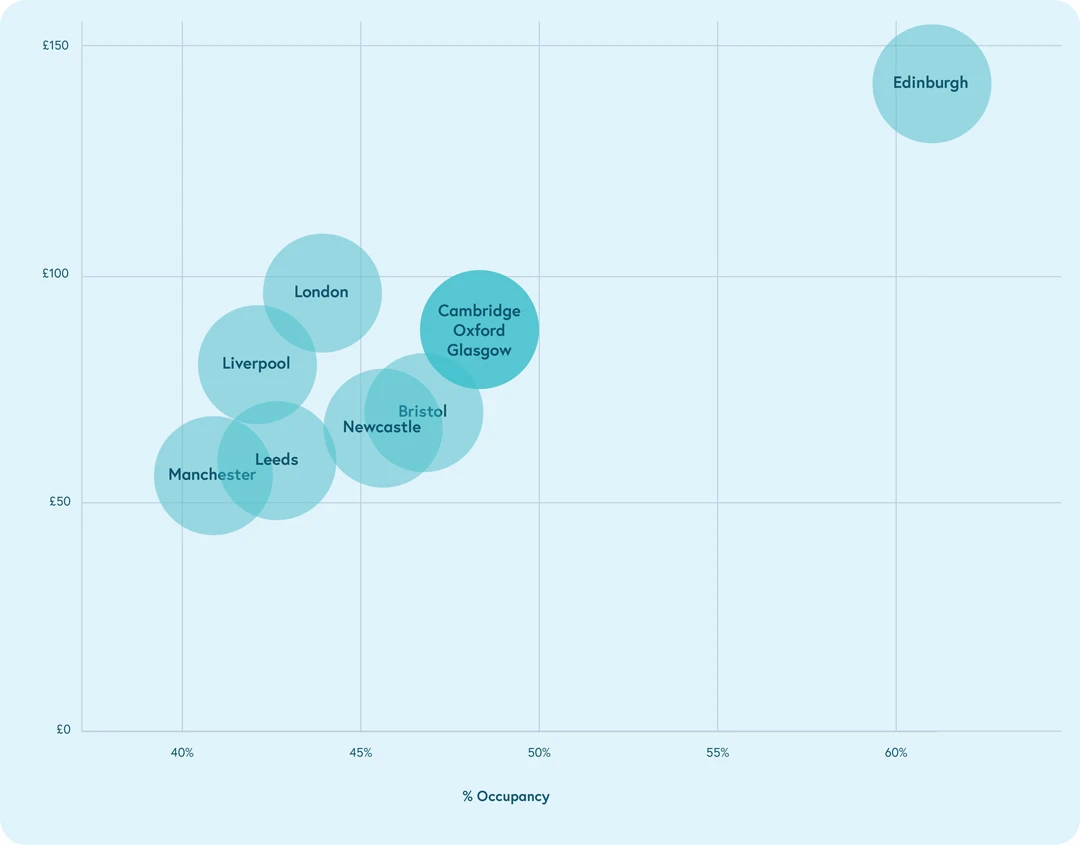

While there were a number of hot markets across the UK, as illustrated in the chart above, Beyond chose to take a deeper look at three markets with the potential for particularly interesting growth. To learn more about what Beyond’s data shows for your specific market,

contact us here.