BLOG TOPICS

2025 Trends in the UK – Tips to Maximise Your Autumn Bookings

.jpg)

September 11, 2025

As the high season draws to a close and “back to school” routines settle in, it’s also the perfect time for property managers and hosts to take a fresh look at their revenue strategies. While guests pack away their summer bags, there’s still plenty of opportunity to maximize the momentum of the past months and prepare for what’s next.

At Beyond, we’ve unpacked the latest shifts in the UK Airbnb market using the most up-to-date data. Our goal: to give you a clear snapshot of how the summer played out, highlight how key performance indicators compare to last year, and—most importantly—share actionable insights to help you refine your short-term strategies and stay ahead of the curve.

Quick Snapshot – 2025 Summer Trends in the UK

The market shows a strong rebound, driven by the summer season and positive signals across all major indicators. Here are the key takeaways:

- Occupancy rate: average occupancy stands at 57%, similar to summer 2024.

- Average length of stay: steady at 6.1 days, with a notable shift towards longer stays (>6 nights) in July and August.

- Summer bookings: travellers are reserving slightly earlier than in 2024 (31 days vs. 33 days).

- Property types: larger homes (>3 bedrooms) and studios remain the most in demand, depending on the period.

- Occupancy year-to-date: down by 5 points compared with 2024

Overall, the indicators suggest that while occupancy remains stable in summer, the demand for longer stays and specific property types is growing. However, the drop in year-to-date occupancy highlights the need for proactive strategies to capture demand outside of the peak season.

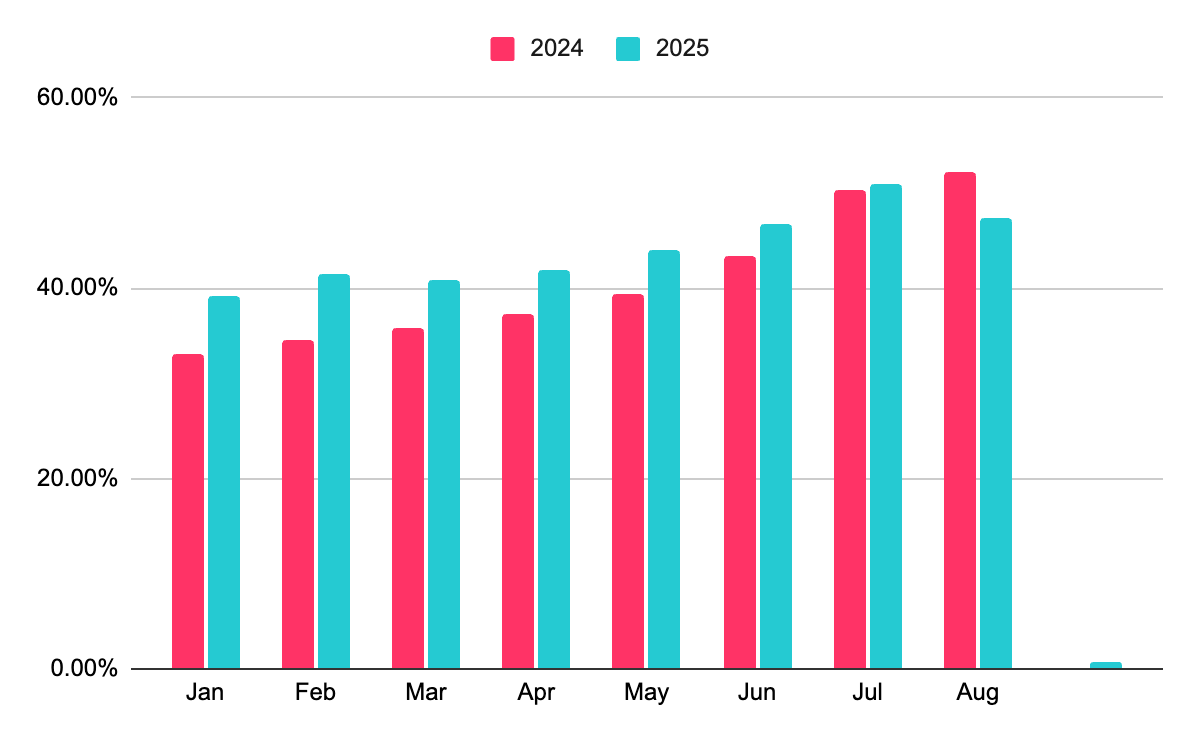

Occupancy pacing: Slightly behind 2024

Occupancy is pacing 1% behind last year. This increase is part of a broader recovery trend that started in the spring. It may also indicate that travellers are booking their stays with shorter lead times. Overall, summer has been particularly dynamic this year.

🎯 Short-term tip:

- Open your calendars further ahead

Travellers plan differently in low season, some book last-minute, but others look ahead to school holidays or autumn getaways. Make sure your calendar is open and visible well in advance. - Optimise pricing dynamically

In the fall season when demand can be lower, adjust your rates smartly instead of applying flat discounts. Use dynamic pricing to reflect seasonality, local events, day-of-week patterns, and real-time demand — raising prices when searches and bookings spike, and offering competitive rates on slower nights. This way, you stay attractive to travellers while protecting your margins. - Leverage local events & experiences

Even outside peak season, cultural events, festivals, or sports competitions drive demand. Update your titles and descriptions to reference these (e.g. “Perfect base for the Autumn Wine Festival”).

Average length of stay: the rise of longer stays in Summer

The average length of stay remains stable at 6 days, the same as in 2024. But this figure hides a clear seasonal trend:

- 45% of bookings in July and August are for stays of more than a week.

- In August, 70% of stays last longer than 6 nights.

- In autumn, 30% of bookings are for just 1 to 2 nights, showing a concentration of short stays outside the peak season.

🎯 Short-term tip:

- Be flexible with minimum stays in autumn. Adjust your minimum stay requirements to match demand outside the peak season. In autumn, consider allowing shorter bookings during quieter weeks, but keep the option to encourage 6-night stays when demand is stronger, — helping you balance occupancy with efficiency.

- Promote longer stays. Highlight weekly or monthly discounts. These are attractive to digital nomads, retirees, or families looking for affordable longer breaks. Longer stays also reduce changeover costs.

- Highlight amenities that suit longer stays, such as a fully equipped kitchen, washing machine, and workspace for remote working.

Property types: the return of small homes

Properties with fewer than 3 bedrooms are particularly in demand during autumn. This reflects a strong trend towards travel in small groups or solo, often for professional trips.

In the UK, the longer average stay in studios in January is likely driven by business travel, academic term starts, and the appeal of affordable city breaks during the off-peak season.

🎯 Short-term tip:

- For larger homes: highlight capacity, family-friendly kitchens, child-friendly amenities, or features such as a BBQ.

- For studios: position them for short stays in the fall season and emphasise their suitability for “city breaks”, professional stays or “student stays.”

Occupancy Rates in Recent Months: On the Rise

Occupancy rates this year are up by an average of five percentage points compared with 2024, signaling a healthy boost for property managers. This positive trend can largely be attributed to stronger demand, with travellers booking earlier and extending winter breaks as well as locking in spring getaways ahead of schedule. At the same time, there’s a clear shift towards off-peak travel, as guests increasingly choose shoulder seasons to sidestep peak prices and crowded destinations—helping sustain occupancy well beyond the summer months.

🎯 Short-term tip:

- Boost your listing appeal with small perks

Add low-cost extras that make a difference in off-peak months — free late checkout, complimentary coffee/tea, or a welcome basket with local products. - Improve your visibility across channels

Consider refreshing photos, updating keywords, and making sure your property appears attractive in the OTAs’ search results. When demand is lower, standing out visually matters even more. - Target new guest segments

Think beyond holidaymakers: remote workers, couples looking for a quiet retreat, or locals booking weekend breaks. Tailor your messaging to highlight what appeals to them (good Wi-Fi, peaceful location, cosy amenities).

Average Daily Rates (ADR): something to keep a close eye on in the upcoming editions.

Average Daily Rate (ADR): a -9% decline, to be monitored closely in upcoming reports

ADR (Average Daily Rate) is a key indicator to track month by month in future updates. This KPI has fallen by 9%, making it a crucial lever to assess:

- Whether the drop in rates is offset by stronger occupancy or overall revenue growth

- The extent to which market demand is putting downward pressure on pricing

- Opportunities to refine your pricing strategy (e.g. by season, events, or length of stay) to limit losses and safeguard profitability

What to Expect This Autumn

As the summer peak winds down, the UK short-term rental market is shifting towards a more balanced and competitive autumn season. While demand is softening compared to summer, several trends stand out that hosts and property managers should prepare for:

- Shorter lead times: Travellers are booking with less advance notice, particularly for weekend getaways or school half-term breaks. Keeping your calendars open and pricing responsive will be key.

- Concentration of shorter stays: Autumn shows a higher share of 1–2 night bookings, reflecting city breaks, professional trips, and spontaneous travel. Flexibility with minimum stays can help capture this demand.

- Increased competition for occupancy: With ADR down by 9%, travellers are more price-sensitive. Success will depend on smart use of dynamic pricing, ensuring you remain competitive on slow days while maximising revenue around events or high-demand periods.

Final Takeaway for Hosts

Autumn in the UK is all about adaptability. To stay ahead:

- Keep your calendars open and competitive, especially for the October half-term and local events.

- Use dynamic pricing to balance real-time demand, seasonal dips, and special events.

- Highlight amenities and positioning (e.g. workspaces, cosy retreats, or city-break appeal) to attract new guest segments outside of the summer holidaymaker profile.

By focusing on flexibility, visibility, and smart pricing, you’ll be better placed to protect your margins and maintain healthy occupancy through the autumn shoulder season.